With energy demand increasing substantially in recent years, energy and utilities companies are preparing for immediate growth opportunities, and they are using mergers and acquisitions (M&A) as a tool to increase operational efficiencies, integrate new technologies, and create greater stability within the sector.

TL;DR:

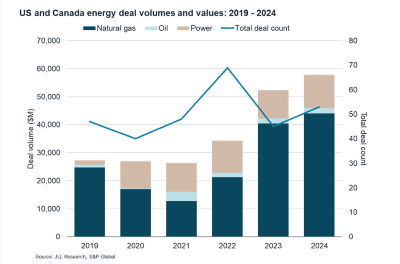

- Energy sector M&A reached $57B in 2024, double pre-pandemic levels

- Deal values are increasing despite fewer transactions

- Natural gas dominates with 60% of deals and 70% of transaction volume

- Strong M&A growth expected to continue in traditional energy subsectors

- M&A consolidation drives both property dispositions and strategic investments as energy companies optimize portfolios and target efficient facilities in favorable regions.

What’s happening? Energy sector M&A is gaining significant momentum, with transaction volumes exceeding $57B in 2024 – more than double the pre-pandemic totals of 2019. This builds on a strong performance in 2023, when energy M&A deals reached $52 billion, an increase of over 50% from 2022.

While the number of completed deals has decreased slightly since 2022, companies are executing higher value transactions as energy demand spikes and increased sector volatility have created increased opportunities for the scaling and modernization of operations.

What’s surprising? The natural gas subsector is leading this growth, accounting for nearly 60% of all completed deals and over 70% of total transaction volume since 2022 (see chart below).

What does this mean for real estate? Consolidation likely means portfolio optimization, as companies will need to rationalize their combined real estate footprints, potentially leading to dispositions of surplus properties but also strategic investments in key locations. Higher natural gas M&A activity may drive demand for specialized industrial facilities, pipeline infrastructure, and office space in energy hubs like Houston, Denver, and Pittsburgh.

Additionally, energy companies pursuing operational efficiencies will seek modern buildings with lower operating costs, and new capital investments may flow to regions with favorable energy policies, infrastructure, and access to resources, creating localized real estate demand spikes.

What’s the outlook? As U.S. policy goals shift, JLL anticipates there will be a continued emphasis on energy M&A activity, particularly within traditional energy subsectors.

Please see the chart below for more information and let me know if you’d to connect with one of our Energy sector experts.

Feature Image Courtesy of: JLL